The ebb and flow

What is critical time?

Time does not flow equally. Regular, sequential, chronological intervals are a fiction. The Greeks called this external linear time chrònos.

Chrònos is an extremely useful fiction for many purposes: for instance, when you wish to coordinate collective action; or when you need a shared language to explain, predict and control natural phenomena.

But external time is as effective when we agree, as it is ineffective when we disagree.

Constructive meaning-making is all about marginal disagreement. Information comes from the fertile differences between our worldviews (and probability distributions). The Greeks had another notion of time: kairos. It represented the eventual now, the right-time right-place kind of moment, the critical opportunity, the exceptional event, the good timing of an action. The time to kill, the time to kiss.

This is very clear in financial markets. As any trade occurs, there are a seller and a buyer "agreeing to disagree" at a certain strike price, expiry, settlement conditions etc. A market tape is just a record of these disagreements. It's like a track of footsteps left in the dark forest of past, present and future decisions. This is why prices (provided they are reached fairly and freely) always carry informational value.

This may sound confusing: how can inter-subjective markets operate with an "inner" time? What is this critical time?

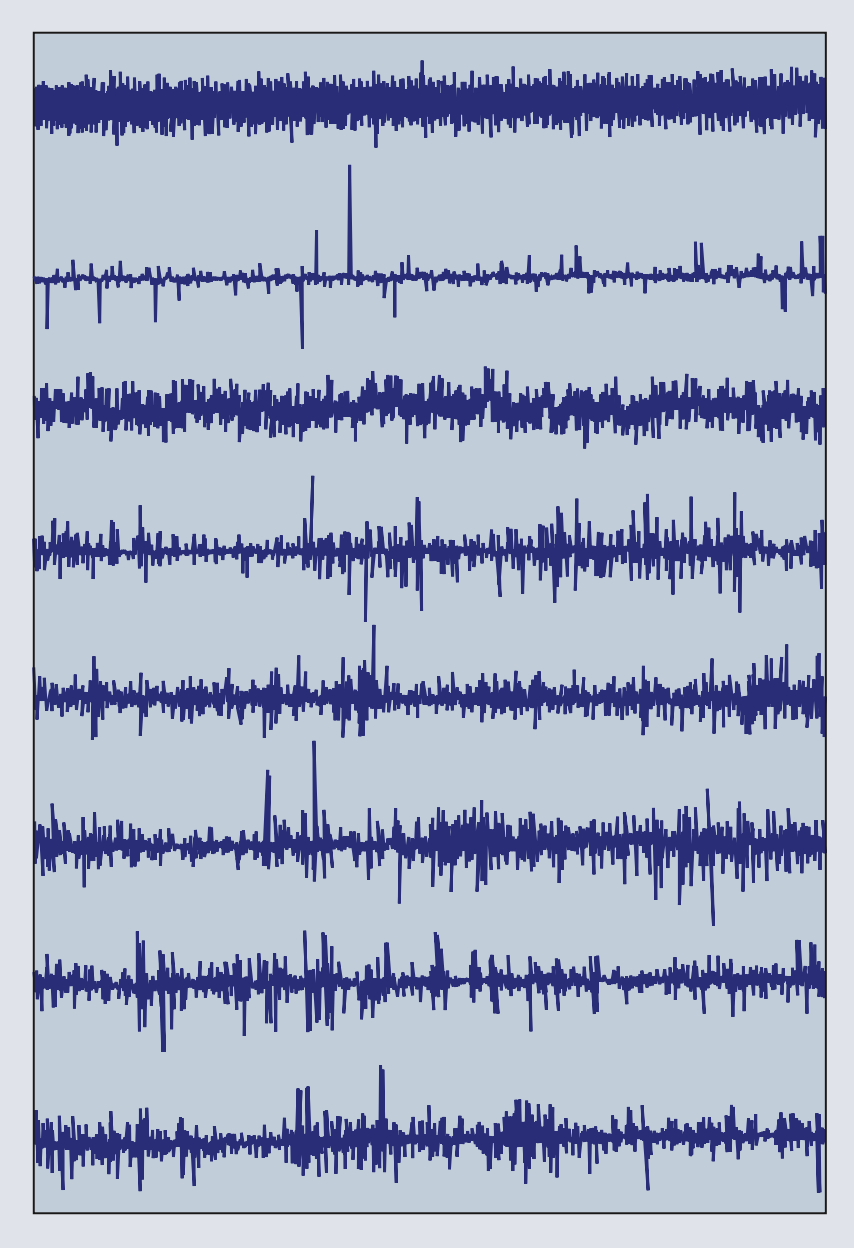

Quick riddle. These graphs illustrate the successive ‘daily’ differences in some actual financial prices and some mathematical models. There is at least one actual time-series. Can you guess which one it is?

Bonus question. What if instead of “daily” differences they were “second” or “weekly” differences? How would you guess change?

Fun fact. 90% of the most commonly used financial models (Sharpe Ratio, Black Scholes, Pearson Correlation … ) assume the first graph is the “real data”…

Take care,

David